Dean Austin, CEO of Austin Benefits Group in Bloomfield Hills, Michigan, is noticing a change in how people treat their health savings accounts.

“I see them paying more attention to HSAs as part of their overall financial strategy,” Austin says. “If people have the financial means—a group with incomes of $80,000 a year and more—we are certainly seeing that they are putting in the maximum contributions and taking the tax benefits.”

That's a change from years past, when consumers contributed about the same amount that they spent in any given year. It's a possible reflection of consumers' growing awareness that they will incur substantial medical costs as they age. In 20 years of retirement, from ages 65 to 85, the average couple will spend about $491,000 out-of-pocket on health care, says Peter Stahl, president of Bedrock Business Results near Philadelphia and an expert on health care challenges during retirement.

Stahl notes that this figure doesn't include time in a nursing home, assisted-living facility or other custodial care. The couple will spend that sum on Medicare premiums, prescription plan premiums, co-pays, home modifications, hearing aids, glasses and sundry other bills.

To fund an expense that can easily balloon above half a million dollars, tax-sheltered medical savings make sense, and they are within reach for affluent consumers in their middle years. In 2015, HSAs will have annual contribution limits of $3,350 for singles and $6,650 for couples, plus a $1,000 additional catch-up contribution allowed each year for those over age 55. (As before, contributions are made in pre-tax dollars.)

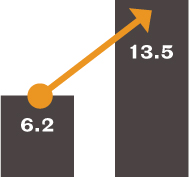

At current contribution limits and an annual return of 4 percent, a couple could begin investing at age 45 and save nearly half their likely out-of-pocket retirement medical expenses by the time they turn 65. Likely increases to annual contribution limits, as well as the $1,000 annual catch-up contribution after age 55, could help them save even more.

The account's earnings are tax free, as long as they are used to pay for items on a long and generous list of medical expenses that include everything from hearing aids to health-related travel. Unlike funds in a flexible spending account, money in an HSA rolls over from one year to the next and so has time to compound and offer returns on investment.

In the past, Stahl says, “most people have thought of HSAs as a way to get a tax deduction and fund items that insurance doesn't cover.” By putting more money in than they spend in a year, or by tapping other funds for out-of-pocket costs, consumers can invest HSA money now and have more—sometimes much more—to spend later.

“If you can fund your medical expenses out of pocket while you are still working, you can reach retirement with a pot of gold socked away in an HSA,” Stahl says.

Interest growing

Complete your profile to continue reading and get FREE access to BenefitsPRO, part of your ALM digital membership.

Your access to unlimited BenefitsPRO content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical BenefitsPRO information including cutting edge post-reform success strategies, access to educational webcasts and videos, resources from industry leaders, and informative Newsletters.

- Exclusive discounts on ALM, BenefitsPRO magazine and BenefitsPRO.com events

- Access to other award-winning ALM websites including ThinkAdvisor.com and Law.com

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.