For all ages, it's imperative to balance near-term and long-termsavings goals, but the makeup of those savings goals has changeddramatically over the past 10 years.

|With the continued rise in health care costs, and increased cost sharingbetween employers and employees, more employees and employers havebeen migrating to consumer-driven health care (CDH) to providelower-cost alternatives.

|With the increased adoption in these plans for employee costsavings purposes, employers have likewise realized similar costsavings to their bottom line. But what role does CDH play in thelong term?

|Related: HSAs could play bigger role in retirementplanning

|The Greatest Generation was able to rely on their pensions,Social Security, Medicaid, and the like as a means to support themin retirement for both medical and living expenses. However, as theBaby Boomers continue their journey towards retirement, relianceupon future proof retirement funds are fading into the sunset forcoming generations. According to a 2015 study from the GovernmentAccountability Office (GAO), 29% of American’s 55 and older do nothave money set aside in a pension plan or alternative retirementplan.

|To make matters worse, some experts are forecasting SocialSecurity funding will be depleted by 2034, leaving even moreretirees potentially without a plan. As such, Generation X andbeyond must look for more creatives measures for savings to make upthe difference.

|In 1978, 401(k) plans were introduced to provide the workforcewith a secondary means for retirement savings while also providingsignificant tax benefits. However, even when actively funded, withrising health care costs and a depleted Social Security system—thesolution this workforce has paid into for their entire career—willnot be enough.

|According to Healthview Services, the average retiree couplewill spend $288,000 for just health care expenses duringretirement. This sum could easily consume one-third of totalretiree savings. This is a contributing factor to the rise andrapid adoption of tax-advantage health accounts to supplementretirement savings. Introduced to the market in 2003, HealthSavings Accounts (HSA) have provided employees with an option toset aside pre-tax funds to either cover current year health careexpenses, like the familiar Flexible Spending Account (FSA), orcarry over the funds year-over-year to pay for medical expenseslater or during retirement. The pretax money employees are able toset aside in these accounts to cover health care expenses, willover time, be on par with retirement savings contributions, such asa 401(k) and 403(b), because of increasing costs and triple-taxsavings.

||It is important for consumers to understand these retirementoptions and how they could be leveraged for greater financialwealth. As a result, the Health Care Stack, an analysis authored byConnectYourCare, acts as a life savings model and illustrates theamount of pretax money consumers can contribute for both theirlifestyle and health expenses in retirement.

|

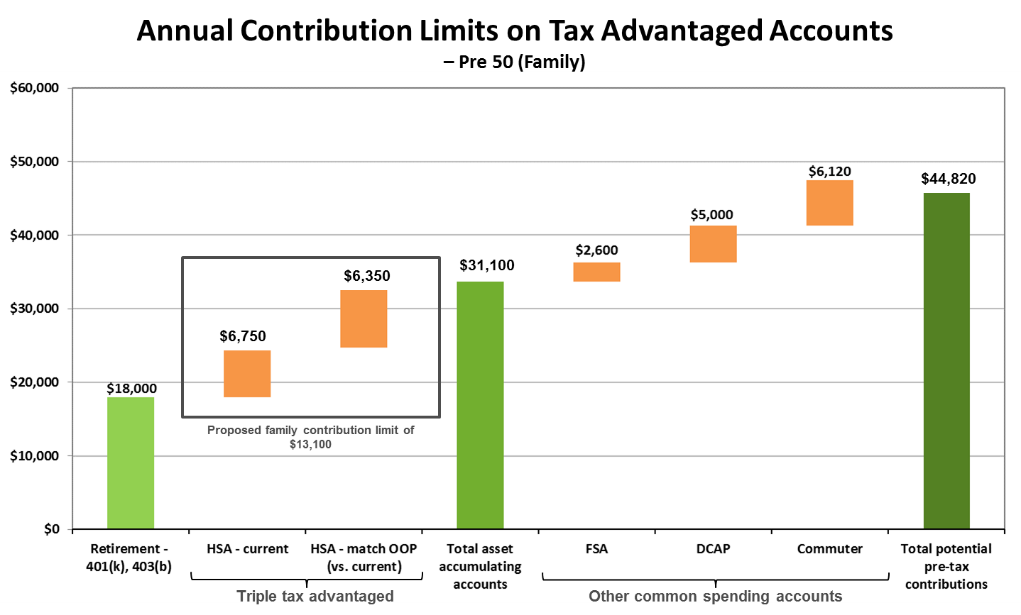

For illustrative purposes, according to current IRS guidelines,the average American under the age of 50 could set aside up to$24,750 each year pre-tax for retirement to cover their health careand living expenses. In this example, if a worker in his or her 30sstarts to set aside the maximum contributions (based on IRSguidelines) for HSA contributions, assuming a rate of return of 3%,they would have $330,000 saved in their HSA to cover health careexpenses once they reach the retirement age of 65. This numbercould be even greater if President Trump’s administration passesany number of proposed bills to increase the HSA contributionlimits to match the maximum out-of-pocket expenses included in highdeductible health plans. This allocation would not only coveraverage medical expenses, but also provide a triple-tax advantagefor consumers from now through retirement.

||In addition to the long-term retirement goals, the yearlypre-tax savings may be even greater if notional accounts arefactored in, with approved IRS limits of a $2,600 per year maximumfor Flexible Spending Accounts, $5,000 per year maximum forDependent Care FSA, and $6,120 per year maximum for commuter plans.This equals $38,470 (or $44,820 if HSA contributions increase) ofpre-tax contributions that consumers could save by offsetting thetax burden and could invest towards retirement.

|

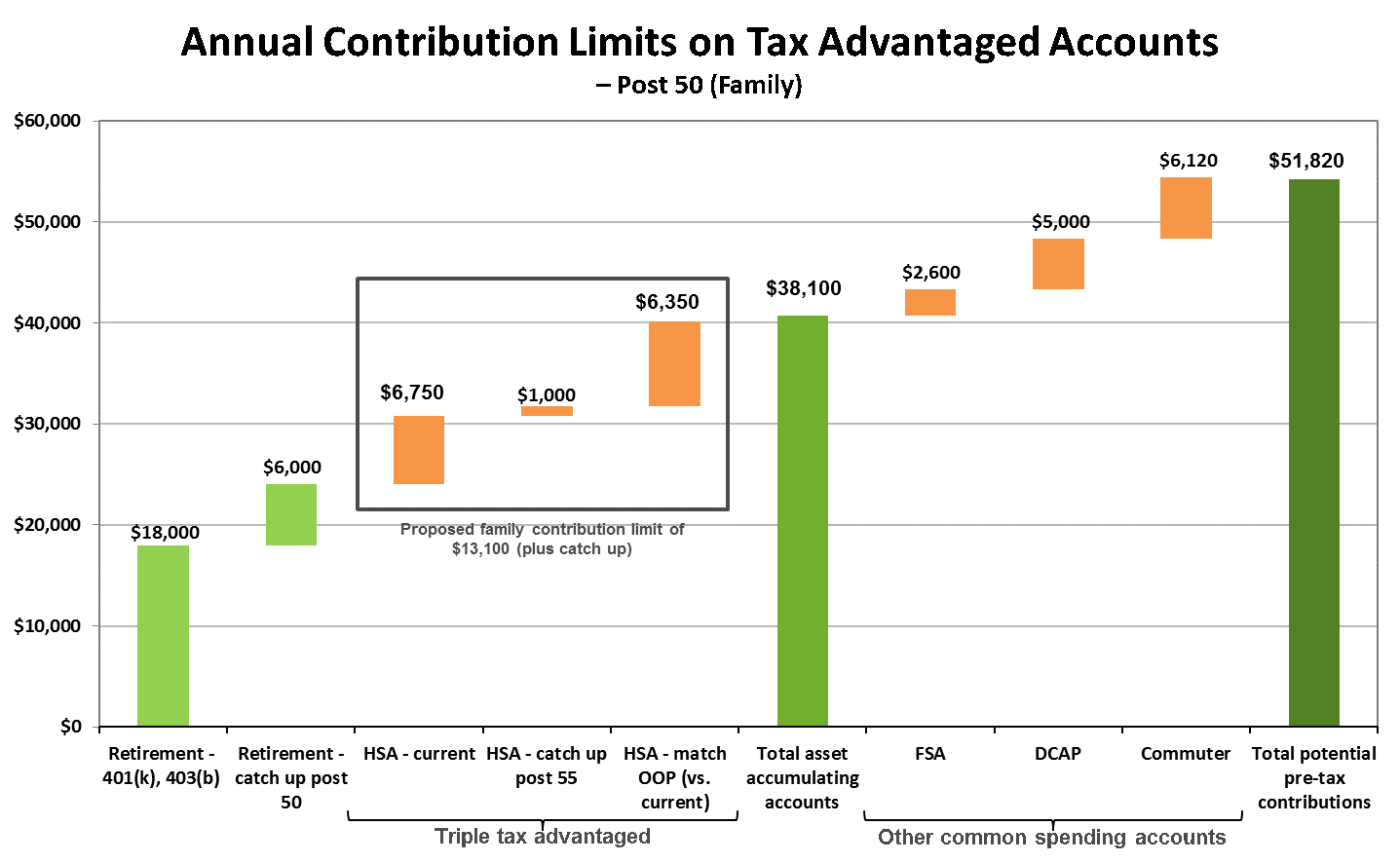

For those consumers over the age of 50, the savings potential iseven greater as they can contribute to a post retirement catch-upfor their 401K plans equaling a total of $24,000, plus they maytake advantage of the $6,750 HSA savings, as well as the additional$1,000 catch up. If certain proposed bills are passed, the increasecould be $38,100 a year that they could set aside, in pre-taxassets, for retirement.

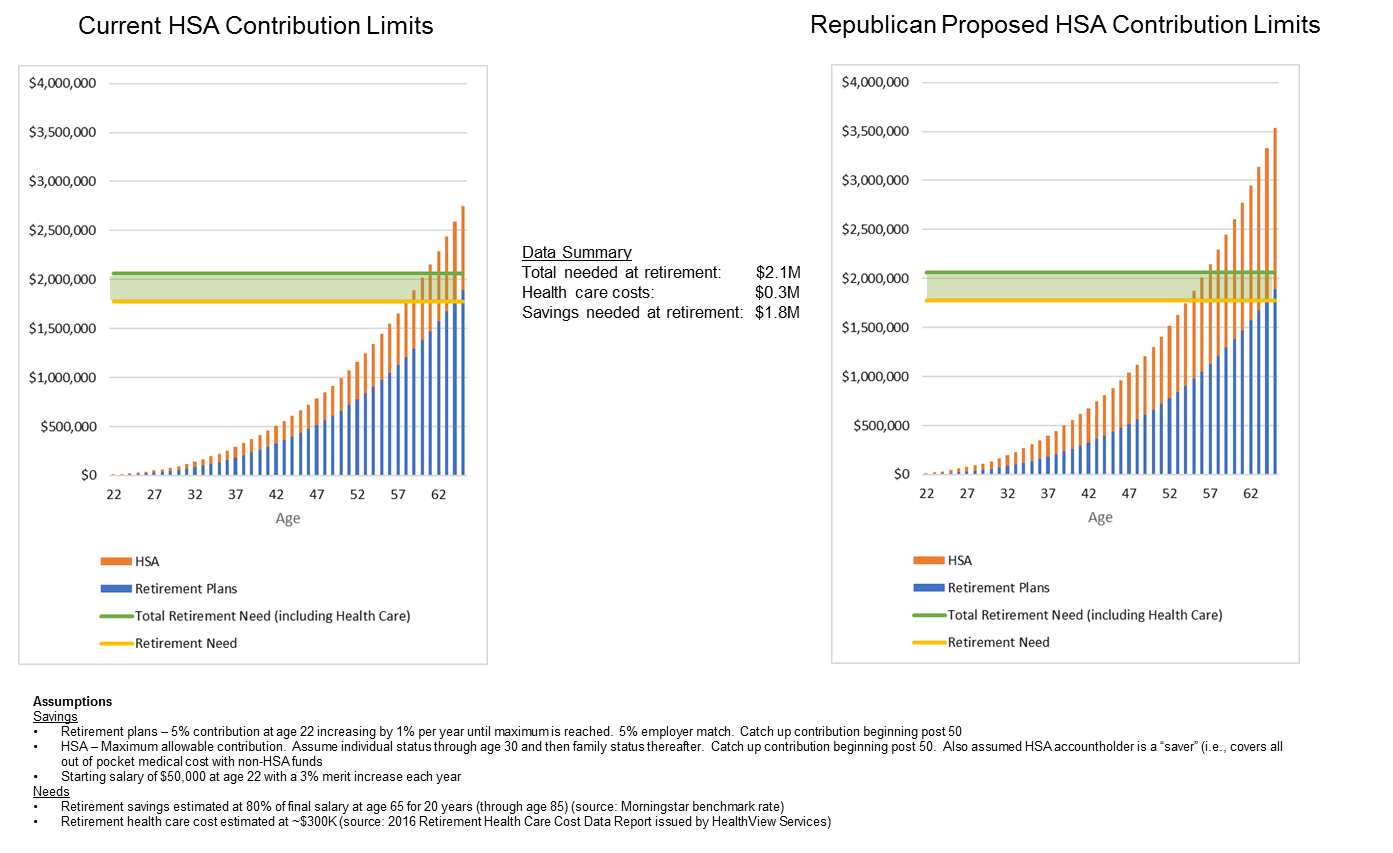

|Not only will an individual’s expenses be covered, but there areother benefits brought forth by proper planning, including thepotential to reach ones retirement savings goals early. Let’s saythat after meeting with a licensed financial investor it wasdetermined that an individual needed $1.8 million in order toretire, and according to national averages, close to $288,000 tocover health care costs.

|

Given the proper investment strategy around contributions toboth retirement and HSA plans, an individual could -theoretically -save enough to meet their retirement investmentneeds by the age of 60 for both lifestyle and health care expensecoverage, if they started making careful investments in their 20s(assuming the worker is making $50,000 per year with a 3% annualincrease).

|In comparison, under current proposals, which include theincreased HSA limits, retirement savings could be achieved evenearlier with the coverage threshold being at 57 for the averageworker. This is a tremendous opportunity to transform retirementinvestment programs for all American workers who would otherwise beleft on their own. Talk about the American dream!

|While there is not a one-size fits all strategy, it is importantfor everyone to understand their options and see how these pretaxaccounts outlined in the Health Care Stack play an importantconsideration in ones future retirement planning.

|Taking the time now to fully understand tax-favored benefitaccounts will provide him or her with the appropriate coverage toenjoy life well into their golden years. Retirement is just aroundthe corner, are you ready?

Complete your profile to continue reading and get FREE access to BenefitsPRO, part of your ALM digital membership.

Your access to unlimited BenefitsPRO content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical BenefitsPRO information including cutting edge post-reform success strategies, access to educational webcasts and videos, resources from industry leaders, and informative Newsletters.

- Exclusive discounts on ALM, BenefitsPRO magazine and BenefitsPRO.com events

- Access to other award-winning ALM websites including ThinkAdvisor.com and Law.com

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.