In 2005, hedge fund manager Michael Burry discovered that the nation's housing market was extremely unstable. He found that high-price tag mortgage loans were being granted to unqualified home buyers. The math didn't work, and he projected that a market collapse was statistically inevitable. When his predictions came to fruition three years later, his $1 billion investment led to a multibillion-dollar return.

This story was famously depicted in Michael Lewis' book and corresponding movie, The Big Short, which tracked Burry and others who identified the inevitable market demise. As depicted in the movie, while the vast majority of Americans believed that the housing market was rock solid, Burry used fundamental financial data to make an investment that went against conventional wisdom.

And like Michael Burry, others who analyze data are witnessing history repeating itself — but in the health care industry.

Like housing, health care is an essential need, and as Michael Burry found in his mortgage data, the math simply doesn't work. Health care costs continue to accelerate and we are approaching a tipping point where they become unsustainable, making transformative change inevitable. Many companies have already reached this point, and eventually, every company will. It's the next bubble waiting to burst.

The numbers behind the bubble

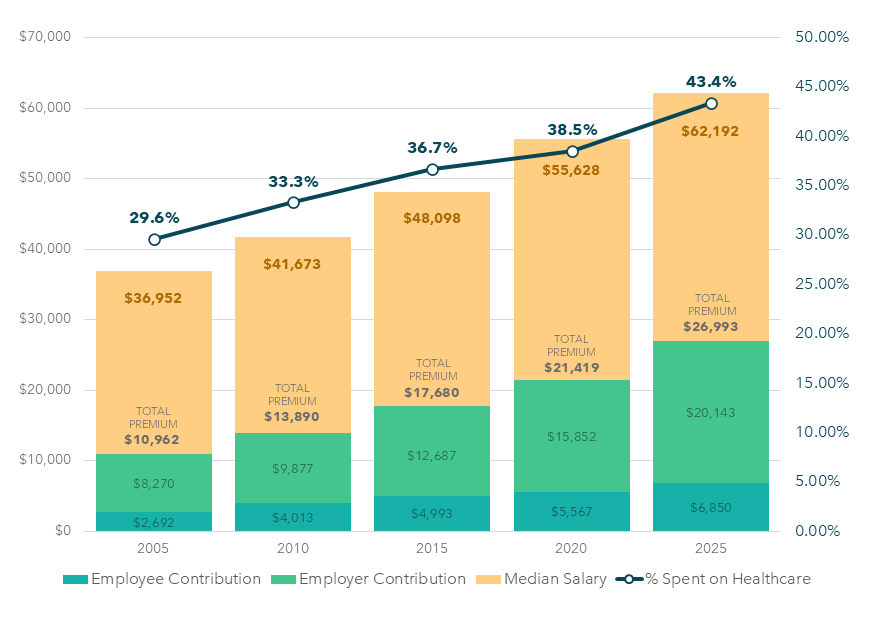

In 2005, while Michael Burry was pouring through mortgage data, an employee's contribution for a family of four's annual premium for health coverage was $2,692. Fast forward twenty years, the employee's contribution for the same coverage was $6,850 — a 154% increase. For employers, their annual contribution to the same plan in 2005 was $8,270, and $20,143 last year — a 143% increase.

This might be manageable if wages and company revenues were increasing at the same rate, but they are not. Wages have increased by 87% since 2004, as a result, the percentage of salary going towards health care premiums has risen from 7.4% to 9.5% (a 28% increase). On top of premium increases, out-of-pocket responsibility has increased 326% since 1999. The huge increase in out-of-pocket expenses leaves many people "functionally uninsured" as they technically have insurance but cannot afford the deductibles. This often leads to finding themselves in collections or avoiding care all together despite having insurance. The impact on businesses is stark as well.

Last year, health plan costs were projected to increase as much as 8% for employers and it ended up even worse. At Imagine360, we heard of many prospective clients facing 30%+ health care renewals. This is on top of increases over the past 20 years that have outpaced national inflation and GDP growth. There is no sign of slowing down and eventually, person by person, company by company, health care costs will reach a breaking point that is untenable. In many cases, it already has. You can only raise deductibles and premiums so high, and you can only have so much of your company's costs tied to medical expenses. The tide is not turning. There are no positive trends — it's only getting worse. This is not a trend that is going be turned by wellness programs or pharmacy vouchers.

So where to look? Costs are driven primarily by rising prices for health care services, which are later passed on to health plans in opaque contract negotiations. The health care facility sets an arbitrary price, the payer negotiates an arbitrary discount, and companies and employees (the ones paying the bills) have no idea what they are being charged or why.

Remember the CDOs in 'The Big Short'? The "collateralized debt obligations" that were so confusing that the film's Director, Adam McKay, used celebrities like Selena Gomez and Anthony Bourdain in real world situations to try to explain them. That's what these contracts are: confusing, inaccessible and impossible for a regular person or executive to have any influence over, which is exactly the point.

Let's say you live in Miami and need a CT scan. Depending on where you go, the billed charges on that same exact scan at different health care facilities could range from $1,843 to $10,551. Same machine, same level of technician, just a mile or so apart. But hey, at least you get that contracted "discount"! And because there are no rules on what the hospitals can charge or what the contracts with carriers need to pay, employers and employees are left with bills that average 2.5x the rate of Medicare nationally. In some states, bills are above 300% of Medicare prices.

Now, before the bubble bursts in health care, it's time for benefits advisors and employers to look at alternative solutions to bring value back into their health plan offerings for employees.

Looking at the data within

There is not one health plan that meets the needs of every employer. Every business and employee population is different. But one thing that is constant is that health care needs to be affordable for both the employer and employee.

Rising costs are ultimately handled by employers in the form of:

- Passing the costs down to employees

- Reducing health coverage

- Absorbing the costs and cutting back in other business areas like staffing, supplies or growth opportunities

All of which are unsustainable for both businesses and their employees and further reiterate the need for benefits leaders to look at alternatives that offer value in health care.

One example is an alternative health plan that uses a reference-based pricing (RBP) approach. Instead of using a pseudo discount off of a make-believe billed charge number, RBP uses a transparent benchmark — often tied to Medicare rates — to determine a fair price for medical services. Then a fair margin is added to ensure equitable reimbursement that works for both sides.

The result? A bottom-ups approach that means employers and their employees understand what they are paying for essential health care services and 20% savings on total health care costs. Outgo the inaccessible CDO-like contracts, and in comes common-sense, transparent payments that will no longer tie to the unsustainable commercial trend increases and closer to the manageable trend of Medicare (2-3%).

When, not if, the pricing bubble finally bursts

"Health care is expensive" is obviously not some new and shocking proclamation. But when you look past just this year's most recent renewal or price hike, and look 10-20 years down the road, there is an inevitable point in time when the math shows the status quo is unsustainable.

The numbers don't lie in this situation: there's a glaring problem with health care costs in our country. There is a trendline pointing increasingly upwards, zooming past inflation, wages and other costs. It's imperative that employers dive deeper into the data and ask questions like: Why do we treat health care as a hands-off expense we can only make small changes to? Can our company withstand five more years of double-digit increases?

Like the increasingly unaffordable housing market that led to a financial crisis in 2008, the cost of health care is on a similar trajectory where the question of the bubble bursting isn't an "if?" It's "when?" And employers shouldn't be caught off guard when maintaining the traditional approach becomes untenable for the business and their employees.

What we do with this information will make the difference. Do employers stand idly by on the sidelines of one of the most pressing problems impacting their business and employees? Or is it time to look at other health plan alternatives that put health care pricing on a course correction?

Companies have a decision to make: Be like Michael Burry, see what's coming and adjust? Or like most people back then, figure it out too late and deal with the fallout. An investor in The Big Short argued that "No one can see a bubble. That's what makes it a bubble." But in health care, it's right in front of us.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.