Look back on 2011, and you'll likely be struck by theextraordinary number of new seeds of innovation that were sown inthe health care industry. Consider:

|The health benefits giant WellPoint purchased CareMore, aninnovative West Coast delivery system that uses prevention andhigh-touch strategies to drastically reduce the cost of caring forfrail elders.

|The Centers for Medicare and Medicaid Services pushed itsinnovation agenda into the provider community with programs toencourage new developments in accountable care, bundled paymentsand local initiatives.

|The human resources consultant and outsourcer Aon Hewittannounced it would create a private health insurance exchange forself-funded large group and national accounts, and then launchedgroups starting this past January.

|A leaked document implied Wal-Mart might be planning to becomethe nation's largest integrated provider of primary care services(a plan the company subsequently pooh-poohed).

|A consortium of Blues purchased Bloom Health, a company thatcreates private exchanges and defined-contribution programs foremployers.

|Meanwhile, providers started taking on greater amounts of risk,to the point of offering insurance products—some independently, andsome with help from some of the largest payers in the country. Andyou couldn't toss a brick without hitting a PCMH pilot program. Toall appearances, the country was on the verge not just of healthreform—but a health care revolution. Based on the headlines, thelong-promised convergence of retail, insurance, health caredelivery and IT seemed just a heartbeat away.

|But this is health care—a garden in which even the hardiestseeds sprout slowly or wither prematurely, and the survivors take apainfully long time to reach maturity. Think of high-deductible,consumer-directed health plans, which were supposed to create ageneration of discerning, value-oriented health care consumers. Orwellness programs with their sticks and carrots to stimulatehealthy behaviors. Or member engagement programs, data exchange andinformatics, and many, many more. To be sure, each of these effortsis having an impact in the market. But they all took time—lots moretime than we first thought.

|In this year's Benefits Selling / Oliver Wyman 2012 Health CareSurvey, we sought to understand what is really happening in themarketplace. Presuming the PatientProtection and Affordable Care Act is implemented on schedule,we're nearing the dawn of public exchanges, essential benefits and more restrictiverating rules. Is the market ready? Will these innovations make itto market in time to have an impact? In this article, we'll sharewhat we heard from nearly 600 agents, brokers and consultantsacross the national marketplace.

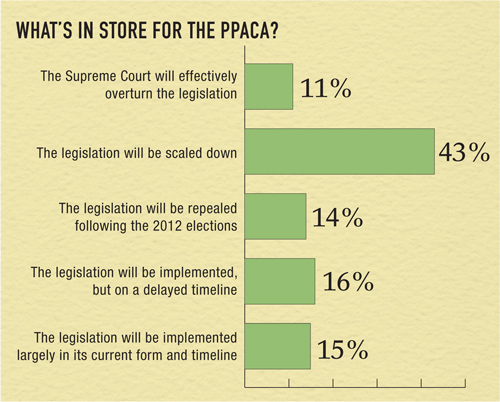

Will 2012 be the end of PPACA?

PPACA will run a gauntlet over the next 12 months. First, itwill be reviewed by the Supreme Court, with an array of potentialoutcomes—including the chance the Court will completely invalidatethe act. Then come the elections in November and the possibilitythat a strong Republican majority could repeal (and likely replace)the act. The channel doesn't expect either of these events. Just 11percent predict the Supreme Court will overturn the legislation,and 14 percent believe that it will be repealed following theelection.

|Most (58 percent) believe that neither event will undo PPACA.Rather, the majority of agents and brokers believe PPACA will beimplemented, but that specific provisions will be scaled down, orthat implementation will be delayed.

|Assuming PPACA moves forward, this year's survey again suggeststhat it will have a profound impact on the channel. Brokers andagents indicate that they will focus less on health insurance andsupportive services such as wellness. As public exchanges attractmembers away from traditional individual and small group plans, ourrespondents expect to see demand for new support services forindividuals and employees. They said they are already thinkingabout shifting their focus to supporting the emerging individualmarket—with compensation being a key remaining question. On thetopic of compensation, this year's results indicate that agents andbrokers continue to feel pressure on their commissions and fees,though the results have not been as dire as they predicted in lastyear's survey.

|

How do exchanges fit in?

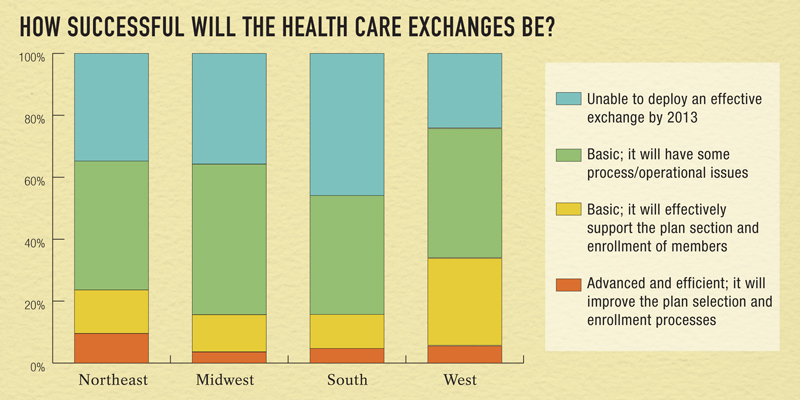

PPACA put exchanges front and center as a new “solution” for amore efficient marketplace. They certainly have grabbed a greatdeal of attention for their perceived ability to create a uniform,competitive marketplace for health benefits, but they have remaineda lightning rod for controversy and are being dealt withdifferently state-by-state. Will they stand up? And, if so, whatimpact will they really have?

|The brokers we talked to were skeptical on both counts. Roughly35 percent said they doubted that public exchanges will beimplemented by the 2014 deadline set forth in PPACA. Another 40percent said exchanges will be created, but will experienceoperational and procedural issues. Not surprisingly, theseperceptions vary geographically—western states taking a morebullish view.

|[Read "Interestin health insurance exchanges grows"]

|Not surprisingly, given these views, brokers were uncertainwhether to recommend the exchanges to their clients. More than halfof brokers serving small groups (fewer than 100 employees) saidthey didn't know whether they would recommend that their groupsmove to the exchange. Interestingly, the small group brokers thathave formed an opinion on the exchanges are twice as likely torecommend them to their clients as not.

|In separate research, employers are taking a similarwait-and-see stance. If the exchanges “work”—that is, if theyprovide employees with a good experience—employers will have a hardtime resisting their efficiencies. But considering the uncertaintythat currently surrounds public exchanges, employers indicate thatprivately run exchanges will likely be the preferred path.

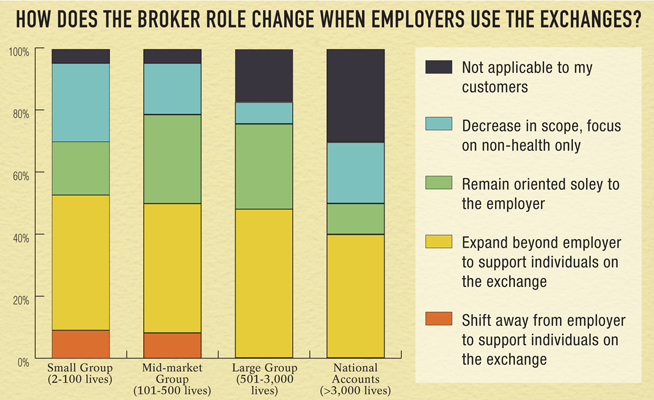

|Does the broker role change with exchanges?

A key questionfor the employer-oriented brokers and consultants: If the marketdoes embrace exchanges, what happens to the role of the adviser?Across the market, from small group to national accounts, roughlyhalf of respondents foresee that their role will shift to includesupport for individuals as they purchase in the exchanges.

A key questionfor the employer-oriented brokers and consultants: If the marketdoes embrace exchanges, what happens to the role of the adviser?Across the market, from small group to national accounts, roughlyhalf of respondents foresee that their role will shift to includesupport for individuals as they purchase in the exchanges.

By contrast, the other half of respondents said their role willremain oriented solely to the employer, and that they will likelyplay a reduced advisory role on health benefits. This is startlingif you think about it. Granted, there is much ambiguity aroundrules, regulations, and compensation—but these responses suggestthat roughly half of the channel is ceding its potential tosupport, guide and influence the purchase of health coverage.

||

What about innovations?

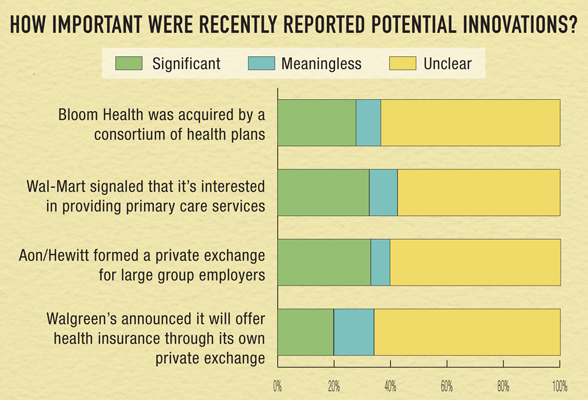

These days, itseems we can hardly make it through the week without some newannouncement—new products and services, new collaborations, newmergers and acquisitions. The news comes from everysector—insurers, providers, technology companies, retailers,financial institutions. But what does it mean? Which developmentsreally count?

These days, itseems we can hardly make it through the week without some newannouncement—new products and services, new collaborations, newmergers and acquisitions. The news comes from everysector—insurers, providers, technology companies, retailers,financial institutions. But what does it mean? Which developmentsreally count?

This year's survey sought to understand the channel'sperspective on four notable events and announcements from 2011,including:

- Walgreen's announcement that it will offer health insurancethrough its own private exchange

- Aon Hewitt's plan to develop a private exchange for large groupemployers

- Reports that Wal-Mart plans to provide primary careservices

- The acquisition of Bloom Health by a consortium of healthplans

While much uncertainty still surrounds these introductions,roughly a third of respondents identified two of them assignificant: the Aon Hewitt private exchange announcement andWal-Mart's (admittedly ambiguous) signal about entering primarycare. On these two announcements, bullish respondents outnumberedtheir bearish counterparts by 4:1 and 3:1.

|Interestingly, the channel regarded the Walgreen's announcementas least significant—with the lowest proportion of respondentssaying that it was significant, and greater balance of bulls andbears. This is interesting in that it seems to indicate thatchannel does not foresee a shift to traditional retailers, holdingapart Wal-Mart's potential foray into care delivery as a clearexception.

|Beyond the headlines, we sought to learn what is reallyhappening on a local level in the transformation to value.Patient-centered medical homes, accountable care organizations,high-performance networks, and value-based benefit designs are allconcepts that have received considerable attention in recent years.Asked about them, the channel responded that it is seeing theadoption of value-based insurance designs, but that providernetwork strategies have yet to really show up in the market.

|Given that some of the national carriers are overtly supportingprovider systems in new insurance product-based commercializationefforts, we suspect that we will see provider-led products gainmomentum in the very near future. One can look to any of a numberof announcements made recently to know that providers will beactively bringing products to market in the near future.

Here we go…

The next 12 months promise to be a roller coaster. In the realmof regulation, the Supreme Court decision, the 2012 election, andstate-level action (or inaction) will set new rules for healthcare. Meanwhile, continued innovation will blur traditional linesbetween stakeholders, and bring a bevy of new products and servicesto market. As the translator and adviser to much of the health caremarketplace, the broker community will play a vital role inconnecting demand for health care solutions to the best options inthe new environment.

Complete your profile to continue reading and get FREE access to BenefitsPRO, part of your ALM digital membership.

Your access to unlimited BenefitsPRO content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical BenefitsPRO information including cutting edge post-reform success strategies, access to educational webcasts and videos, resources from industry leaders, and informative Newsletters.

- Exclusive discounts on ALM, BenefitsPRO magazine and BenefitsPRO.com events

- Access to other award-winning ALM websites including ThinkAdvisor.com and Law.com

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.