|

Government-controlled health carehas been on the minds of benefits advisors for years now, loomingas a distant threat, but often pushed aside for more pressingconcerns. But during the opening keynote of the recent NextGenGrowth & Leadership Summit in Nashville, Nelson Griswold warnedthat the benefits industry underestimates the threat ofsingle-payer at its own peril.

Government-controlled health carehas been on the minds of benefits advisors for years now, loomingas a distant threat, but often pushed aside for more pressingconcerns. But during the opening keynote of the recent NextGenGrowth & Leadership Summit in Nashville, Nelson Griswold warnedthat the benefits industry underestimates the threat ofsingle-payer at its own peril.

Citing a progression from HillaryClinton to Bernie Sanders, and a lack of clarity from PresidentTrump, Griswold, a benefitsindustry thought leader and strategist, discussed the growing momentum around the ideaof Medicare for All, adding that although government-controlledhealth care doesn't generally poll well, everything changes whenyou ask Americans if they're interested in Medicare forAll.

|Related: Poll shows growing support for Medicare forAll

|For example, recent surveys havefound that 70 percent of Americans are open to adopting Medicarefor All, while even 52 percent of Republicans supportit.

|Griswold noted that former AetnaCEO, Mark Bertolini, also weighed in recently, saying “As a nation,I think we should have a debate about single-payer.”

|“As I was growing up,” Griswoldsaid, “the bulwark against the idea of socialized medicine wasalways the doctors. So most concerning of all to me is the factthat 56 percent of doctors now either strongly support or somewhatsupport single payer health care.”

|So what does that mean forbenefits advisors? Yes, a growing number of advisors have made aconscious decision to become consultants rather than insurancebrokers, which would give them an advantage if a major shift shouldoccur. “But this is a fight we don't want to lose,” Griswoldwarned. “Once a country has moved to government-controlled healthcare, it has never gone back. My prediction is that we'll havesingle payer in five years.”

|As attendees let those words sinkin, Griswold examined the factors contributing to this potentialsea change.

|“What's driving people'sfrustration and willingness to embrace a new system?” he asked.“The numbers, of course.”

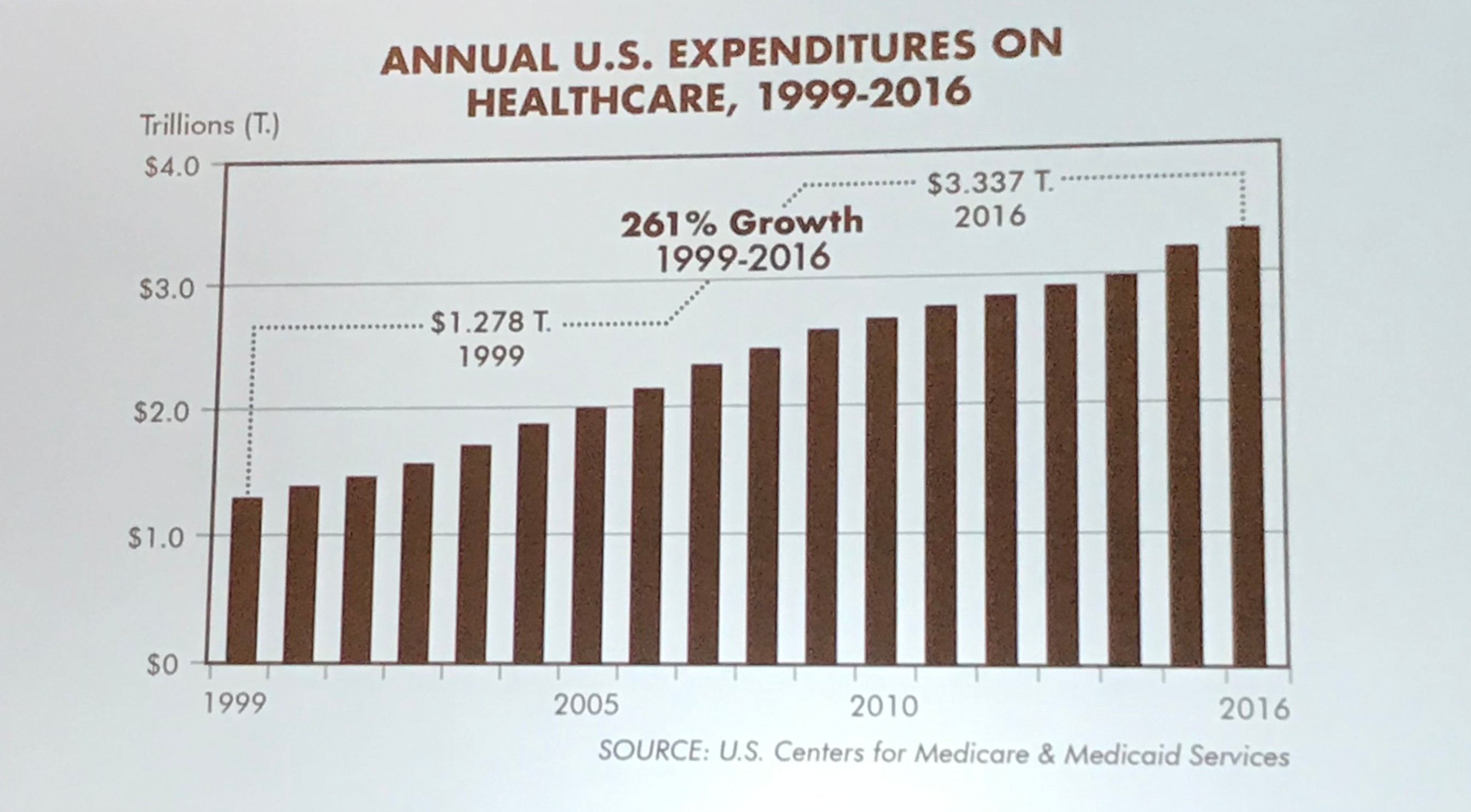

|American health care hasincreased in cost every year since 1960, Griswold said. “In thelast 17 years alone, we've seen 261 percent growth in the cost ofhealth care. Why does it go up every year? We're in a period ofalmost no inflation elsewhere, and yet we've had massive inflationin health care year over year.”

|

Griswold pointed to the rootcause of the problems with American health care identified by JohnTorinus in his book, “The Company That Solved Health Care.” Torinuswrote, “CEOs should beembarrassed at how they have allowed health costs to run wild. Theywould not allow that to happen in any other part of theirbusinesses.”

|Companies manage and negotiateother aspects of their business down to the penny or even a tenthof a penny, Griswold said. “Why wouldn't they do the same with thecost of a heart transplant?”

|Some executives are starting toget it, but it's been a very slow awakening. “Why is the C-suiteignoring their second or third largest cost set?” he asked. “Why dothese otherwise brilliant and business-savvy people refuse to lookat health care?”

|“I believe it's due to somethingI call health care's big lie. This lie has been told over and overto CEOs and CFOs until they believe it.”

|What's the big lie? “Mr. and Mrs.CEO/CFO, you have no control over the cost of your health care.There's nothing you can do to influence it and it will increaseevery year. So will your health care premiums. You must learn tolive with it. We'll do our best to manage it, but there's nothingwe can really do either.”

|Griswold said this idea creates awall that separate two groups that should be talking: the payer(employers or individual patients who are paying) and the providers(doctors, hospitals and drug companies). The wall means there's nocommunication, other than providers throwing claims statements overthe wall and the payers throwing cash back the other way, Griswoldsaid.

|The buyers aren't watching thesellers and no one is managing health care as a purchase. Hospitalsmanage their supply very closely, but their customers—theemployers—don't. And neither do their employees, Griswoldsaid.

|But what is the wall? Accordingto Griswold, it's “carriers and status quo brokers” who maintainthe lie that nothing can be done.

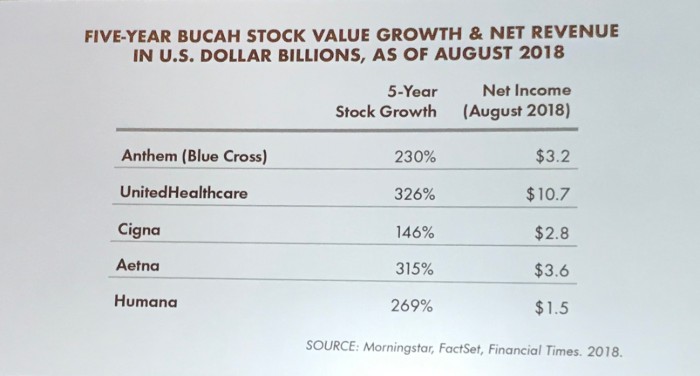

|Despite the upheaval in healthcare post-ACA, the carriers continue to do very well, as evidencedby their revenue numbers, he said.

|

“When an insurance company'srevenue goes up, what drives their revenue?” Griswold asked.“Premium. When health care drives up the cost of premium, revenuegoes up for insurance companies.They have no incentive to lower thecost of health care and every incentive to prevent employers fromdoing so.”

|Griswold added that theirpartners in crime, often unaware of their role, are status quobrokers. If a client's premium goes up, they get araise.

|The current cycle of massiveincreases every year is unsustainable, he said. “The system willcollapse. Single-payer is looming and companies and their employeeare paying more and more all the time.”

|The only hope, according toGriswold, is a “benefits revolution” that is already underway. Itis gaining momentum due to the frustration that'sspreading throughout the health care and employee benefits worlds.“As an advisor, when it becomes a victory to deliver the least badnews, it sucks the life and joy of your business.”

|The goal of the revolution is toaddress the misaligned incentives that exist in the current system.So what's the strategy? “To reinvent U.S. health care from theinside out in order to lower and control the cost of health careand make single-payer health careunnecessary.”

|To be successful going forward,he said, advisors need to change what they sell, who they sell itto, and how they sell.

|Also read: Breakaway brokers

|Instead of selling insurance,they need to sell strategy, solutions, results and the supply chainmanagement of health care. In other words, controlling and managingthe quality and cost of the health care employees purchase undertheir employer sponsored health care.

|Why does what advisors sell haveto change? Because what they've sold before doesn't address the topcost drivers: prescription drugs, hospital, outpatient surgery andphysician visits.

|The strategies, tactics andsolutions providers that will help drive these costs down arealready out there, Griswold noted. They include medical management,reference-based pricing, direct primary care, and directcontracting, among others.

|And while brokers used to sell toHR because they manage benefits, they now need to work directlywith the C-suite. Why? “Because they own the profit and lossstatement and give a damn whether costs are cut. That's not in HR'sjob description.”

|Members of the C-suite are theones who are willing to make big changes because they care aboutbig results and how it could impact the bottom line, Griswoldsaid.

|Why do benefits advisors need tochange? Because consultative questions allow you to identify painpoints. You have to probe and be precise. Consultants solveproblems; salespeople sell products and services. And those whomake these changes will have a tremendous competitive edge,Griswold said.

|“Single-payer and Medicare forAll aren't going away,” he concluded. “The idea has been chippingaway at the body politic for decades. This should scare you, but wehave an opportunity to stop single-payer in its tracks withstrategies that do to health care costs what government controlpresumes to do.

|“If you don't help your clientsmanage the cost of their health care over the next five years,”Griswold said, “send me a note letting me know about your newcareer. What do you want to do next? You have an opportunity tohave a dramatic impact.”

Complete your profile to continue reading and get FREE access to BenefitsPRO, part of your ALM digital membership.

Your access to unlimited BenefitsPRO content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical BenefitsPRO information including cutting edge post-reform success strategies, access to educational webcasts and videos, resources from industry leaders, and informative Newsletters.

- Exclusive discounts on ALM, BenefitsPRO magazine and BenefitsPRO.com events

- Access to other award-winning ALM websites including ThinkAdvisor.com and Law.com

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

Paul Wilson

Paul Wilson is the editor-in-chief of BenefitsPRO Magazine and BenefitsPRO.com. He has covered the insurance industry for more than a decade, including stints at Retirement Advisor Magazine and ProducersWeb.