As defined contribution plans evolve, so too must the investment options that support participants on their retirement journeys. Nearly 6 out of 10 plan sponsors are focused on evaluating their investment lineups holistically, according to an MFS DC Plan Sponsor Survey of 166 U.S. plan sponsors conducted in 2024.

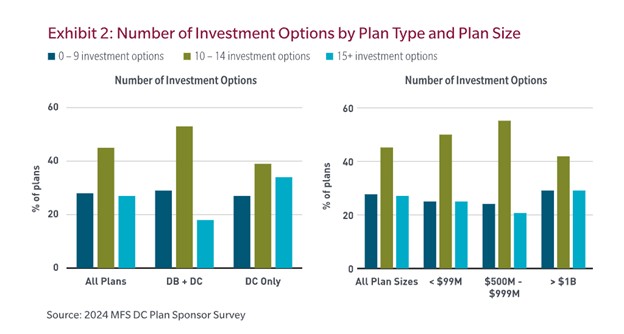

The typical DC investment menu is comprised of generally 10 to 14 investment options broken out into three tiers. Tier 3 is made up of non-core options such as a brokerage window, company stock, and alternative investments that have been garnering a fair amount of attention after President Trump issued an executive order in August aiming to ease access to private market investments in defined contribution plans.

Yet it's important to consider all parts of the menu, especially when Tier 1, with qualified default investment alternatives including TDFs, and Tier 3, are getting the lions' share of attention these days. Tier 2 represents the core investment options available to participants, which are predominantly traditional equity and fixed income options. Nearly all plans report having bond funds as well as domestic and international equity options available in their plan menus. Approximately 70% of plans have a capital preservation option, either money market or stable value.

NEPC's 2024 DC Plan Trends and Fee Report found that in the most streamlined menus, it is most common to have 0-1 cash options, 0-1 bond options, and 0-3 stock options. For plans with larger core investment menus, it is most common to have 1-4 cash options, 1-4 bond options, and 5-10 stock options.

Tier 1 consists of the Qualified Default Investment Alternative (QDIA), the investment option within a plan where contributions automatically are directed when the participant fails to make their own investment choices. Within this tier, target date funds (TDFs) are the most prevalent QDIA and have grown in popularity over the last 20 years, reaching a new high of $4 trillion in assets in 20242. Through the rise of automatic enrollment and escalation, participant usage of TDFs continues to climb, especially among younger employees.

The NEPC report indicated that 86% of participants under 35 invest only in target date funds and that 64% of contributions for that demographic are directed to TDFs. However, these statistics decline with age. The same survey found that for participants over 65, only 58% solely invest in target date funds, with only 54% of contributions directed towards TDFs. Accordingly, older participants tend to hold and make contributions to investments in the core menu.

The growth in target date users and assets has driven a corresponding decline in core menu assets, with 54% of all DC plan assets invested in core menu options as of the end of 2024, down from 72% in 2011.

Innovations in investment menu design: What's next?

There have been two persistent and prevalent trends in investment menu design that sponsors have been considering for more than a decade. The first is decumulation, and what role retirement income solutions should play in helping participants draw down their retirement assets. The second is customization and/or personalization via customized target date funds and managed accounts that can be personalized at the plan and/or the individual level. We believe both trends have important implications for the future of the core menu.

Decumulation: Do you have the right options to entice retirees to stay in plan?

This increasing focus on decumulation strategies reflects a shift toward providing participants with options to manage retirement income directly within the plan. This shift could impact the core menu's structure, potentially introducing new options tailored for longer-term engagement and income management.

Today, sponsors are being challenged to contemplate retirement income solutions for their participants, including complex solutions that lengthen the fiduciary relationship, increase cost and have not truly been tested by the market. Our plan sponsor survey confirmed that sponsors are taking a cautious approach to this space, with only 15% of plan sponsors likely to implement a retirement income solution in the next 12 to 18 months.

By thinking more creatively about the mix of investment options in the core menu and aligning plan design to allow for more flexibility with distribution options, there is plenty a plan sponsor can do to help participants decumulate their assets and create meaningful retirement income without the need to incorporate complex retirement income solutions.

We know most plans offer a capital preservation option, with 53% indicating they offer stable value and another 28% indicating they offer both stable value and money market options. Our survey showed 81% of plan sponsors believe stable value looks to provide broad capital preservation and is a solution that can be used in both the accumulation and decumulation stages. Beyond capital preservation, we believe having the right array of conservative fixed income options, including shorter duration fixed income, will be critical for retirees who wish to decumulate their assets from the plan.

From a plan design perspective, we believe sponsors should consider distribution options such as systematic withdrawals or partial distributions so participants can take ongoing or periodic distributions from the plan in retirement. On the education front, offering tools and services, including education around Social Security and claiming strategies, may also be beneficial for participants.

The opinions expressed above are those of the authors and do not necessarily reflect those of MFS.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.